Facing financial uncertainty can be stressful, especially when you worry that the assets you’ve worked hard for could be at risk from creditors or a lawsuit. The key to protecting what’s yours is knowing how to protect assets from creditors before a problem arises, using the legal tools available right here in North Carolina.

Your Guide to North Carolina Asset Protection

When people hear "asset protection," they often think it's a complicated strategy just for the extremely wealthy. The reality is, it’s a core part of smart financial planning for anyone in North Carolina—from small business owners and medical professionals to families simply planning for their future.

The goal isn't to hide money or illegally dodge legitimate debts. It's about legally and ethically structuring your finances to shield your property from potential future claims. Without a solid plan, a single unexpected lawsuit, business downturn, or medical emergency could put everything you've built in jeopardy.

Why Proactive Planning Is Essential

In asset protection, timing is everything. The most powerful strategies are only effective if you put them in place before a creditor shows up. Trying to move assets after you've been sued or have already incurred a major debt is a huge red flag. It can be viewed as a fraudulent transfer under North Carolina law, which can unwind the protection and create even bigger legal problems.

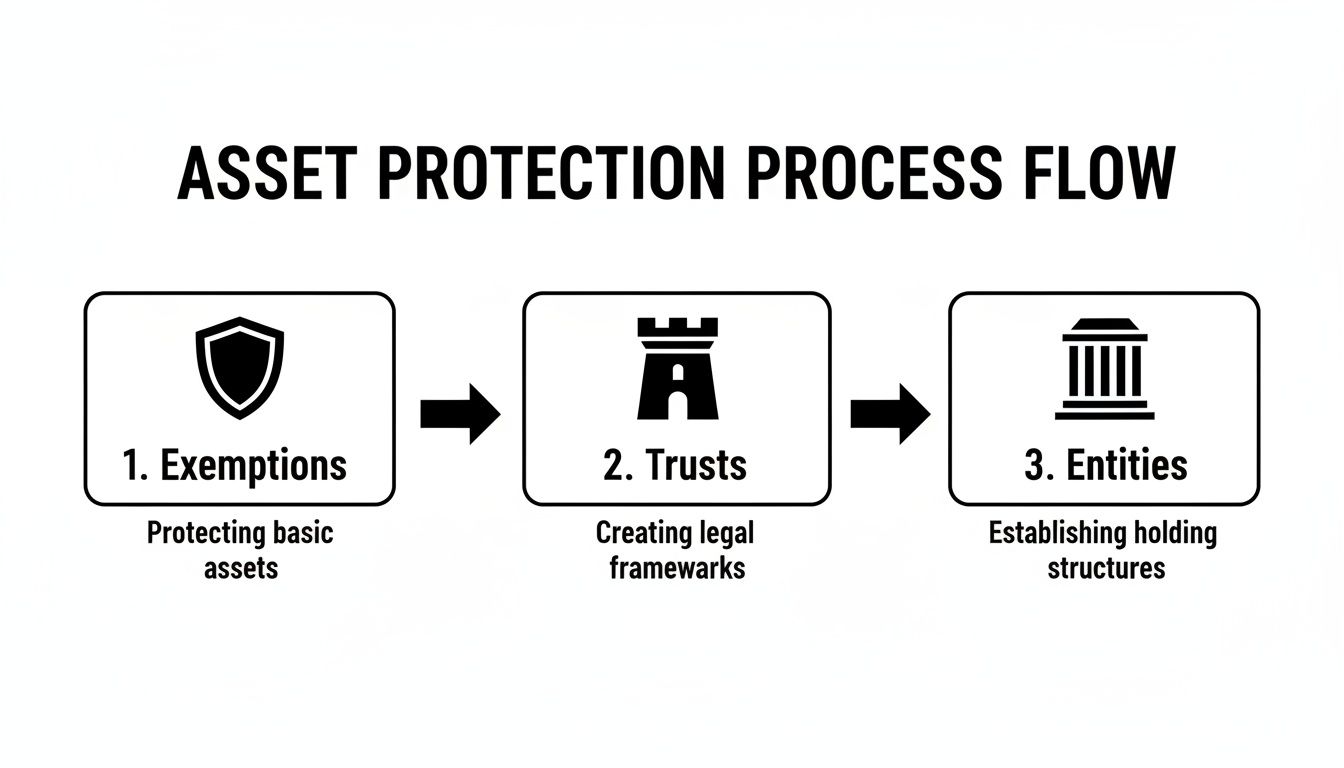

By planning ahead, you can take full advantage of North Carolina's legal framework. The main tools we use include:

- Statutory Exemptions: North Carolina law automatically protects certain assets up to specific values from creditors.

- Trusts: These legal structures hold and manage assets on your behalf, often placing them beyond the reach of your personal creditors.

- Business Entities: Forming an LLC or corporation is critical for creating a liability shield that separates your business debts from your personal finances.

This chart breaks down the core strategies we use to build a protective wall around our clients' assets.

The best approach often involves layering these tools. We start with fundamental exemptions and then add more sophisticated trust and business structures to create a comprehensive defense tailored to your situation.

A sound asset protection strategy isn't a standalone fix; it's woven directly into your overall financial management and estate plan. The following table provides a clear summary of how these key methods work together to safeguard different types of assets under North Carolina law.

Key Asset Protection Methods in North Carolina

| Asset Type | Protection Method | Primary Benefit in NC |

|---|---|---|

| Personal Residence | Homestead Exemption & Tenancy by the Entirety | Protects up to $35,000 in equity (or $70,000 for married couples) and shields property from the debts of one spouse. |

| Retirement Savings | ERISA & State Exemptions | Federally-protected accounts (401(k)s, pensions) and state-protected IRAs are shielded from creditors. |

| Cash, Investments | Irrevocable Trusts | Moves assets out of your personal ownership, placing them beyond the reach of future personal creditors. |

| Business Interests | LLCs & Corporations | Creates a "corporate veil" that separates business liabilities from your personal assets. |

| Personal Property | Statutory Exemptions ("Wildcard") | Protects a specific dollar amount for vehicles, household goods, and a "wildcard" for any other property. |

By using these tools strategically, you can create a robust defense that aligns with your long-term goals.

A Foundational Part of Your Financial Health

Ultimately, good asset protection is about securing your family’s future. It ensures the wealth you’ve created is preserved for your heirs, not lost to an unexpected creditor or lawsuit. A well-designed plan gives you peace of mind and control over your financial legacy. To see how these strategies fit into a larger plan, you can explore our overview of North Carolina estate planning.

Using North Carolina Exemptions to Shield Your Property

When a creditor has a judgment against you, it’s easy to think you’ll lose everything. But North Carolina law doesn't leave you defenseless. The state provides a powerful set of legal tools called exemptions that act as a first line of defense for your most important assets.

These exemptions are not loopholes; they are legal shields created by statute to protect specific property up to a certain value from being taken by most judgment creditors. If someone wins a lawsuit against you, these laws ensure you can keep the essentials needed to live and work. Think of them as a protective bubble around your core assets.

The North Carolina Homestead Exemption

For most people, their home is their biggest investment and their greatest source of stability. North Carolina’s Homestead Exemption, found in North Carolina General Statute § 1C-1601(a)(1), is designed to protect it.

This law allows you to shield up to $35,000 of equity in your primary residence from creditors. If you're married and own the home together as "tenants by the entirety," that protection doubles to $70,000 against a joint debt. The law also provides an increased exemption of $60,000 for unmarried individuals 65 or older whose spouse has passed away, as long as they previously owned the property together.

Real-World Scenario:

Take Sarah, a Raleigh small business owner whose venture didn't succeed, resulting in a personal judgment of $50,000 against her. Her home is worth $300,000, but she still owes $270,000 on her mortgage. This leaves her with $30,000 in home equity. Because her equity is below the $35,000 homestead exemption limit, a creditor cannot force the sale of her home to satisfy the judgment.

Key Insight: The homestead exemption protects your equity—the difference between your home's market value and your mortgage balance—not its total value. This is a foundational piece of asset protection for homeowners across North Carolina.

Protections for Personal Property and Vehicles

Beyond your home, state law also recognizes that you need other assets to function day-to-day. Exemptions are in place to protect your vehicle, household belongings, and other items you need to maintain your life and livelihood.

Here are some of the key personal property exemptions you should know:

- Motor Vehicle Exemption: You can protect up to $3,500 in equity in one vehicle. If you own a car worth $3,000 outright, it's completely safe from seizure.

- Household Goods: This covers furniture, clothing, appliances, and books. You can protect up to $5,000 for yourself, plus another $1,000 for each of your first four dependents. A family with two kids could shield up to $7,000 in household items.

- Tools of the Trade: If you need certain equipment, books, or tools for your profession, you can protect up to $2,000 worth.

The Versatile "Wildcard" Exemption

One of the most powerful and often-overlooked tools in the North Carolina exemption playbook is the "wildcard" exemption. This flexible protection can be applied to any property not already covered by a more specific exemption.

Under N.C.G.S. § 1C-1601(a)(2), any unused portion of your $35,000 homestead exemption can become your wildcard. This is a game-changer, especially for renters or those with low home equity.

For instance, if you only have $10,000 of equity in your home, you have $25,000 remaining from your homestead exemption. That $25,000 can be used as a wildcard to protect a second car, cash in a savings account, or a valuable family heirloom. If you don't own a home at all, the entire $35,000 becomes available to shield your other assets from creditors.

Using Retirement Accounts to Shield Your Assets From Creditors

For most people in North Carolina, a retirement account is the largest asset they own, built over a lifetime of work. The good news is that these accounts have some of the strongest legal protections available, making them a powerful tool for shielding your wealth from creditors.

Think of it as a double-layered shield, with protections coming from both federal and state laws. Understanding how these work together is the key to feeling confident about your financial future.

The Federal Shield: ERISA-Qualified Plans

The Employee Retirement Income Security Act of 1974 (ERISA) is a landmark federal law that creates a powerful safeguard for most employer-sponsored retirement plans. This protection covers the accounts most people are familiar with:

- 401(k) and 403(b) plans

- Pensions

- Defined-benefit plans

Under ERISA, the money inside these plans is practically untouchable by everyday judgment creditors. If you get sued over a business dispute, a car accident, or even credit card debt, creditors can’t come after your 401(k). The protection is nearly absolute, except in specific cases like IRS tax liens or divorce orders.

Key Takeaway: ERISA-qualified plans offer one of the strongest forms of asset protection out there. This means maximizing your 401(k) contributions isn't just a smart retirement move—it's also a simple and highly effective asset protection strategy.

The sheer scale of these protected funds underscores their importance in personal finance. As the global pension market report shows, pension and defined contribution plan assets have grown to staggering levels. Because of ERISA, these funds are almost completely off-limits to creditors.

North Carolina’s Strong Protections for IRAs

So, what about retirement accounts that aren't tied to an employer, like a Traditional or Roth IRA? These accounts aren't covered by federal ERISA law. Instead, their protection comes from the state—and thankfully, North Carolina provides incredibly robust safeguards.

Under North Carolina General Statute § 1C-1601(a)(9), your individual retirement accounts are fully exempt from creditors. There is no dollar limit. Whether you have $50,000 or $1 million in your IRA, the entire amount is protected.

Real-World Scenario:

Imagine a physician in Charlotte who operates as a sole proprietor and is rightly concerned about potential malpractice claims. She has $750,000 in her personal IRA. Because North Carolina law offers an unlimited exemption, those funds are completely safe from a malpractice judgment. Her retirement is secure, no matter what happens in her professional practice.

This unlimited IRA protection gives North Carolina residents a significant advantage, allowing them to build their nest egg with peace of mind.

Important Exceptions and Common Pitfalls

While these protections are powerful, they aren't completely without limits. It's crucial to understand a few key exceptions to avoid any surprises down the road.

The most common area of confusion is divorce. While your 401(k) is safe from a creditor your spouse might have, the account itself is considered marital property. A judge can order it to be divided in a divorce through a Qualified Domestic Relations Order (QDRO). This isn't a creditor claim; it's a family law obligation to distribute marital assets fairly.

Additionally, a few powerful creditors can bypass these protections:

- The IRS: The federal government has the authority to levy retirement accounts for unpaid tax debts.

- SEC Actions: In cases involving securities fraud, the SEC can go after retirement funds.

- Federal Criminal Fines: Certain federal criminal penalties can also expose these assets to seizure.

For the vast majority of people facing common civil debts, however, retirement accounts are a financial fortress. Planning your contributions wisely is one of the simplest and most effective ways to protect the assets you've worked so hard to build.

Building a Financial Fortress with Trusts and Estate Planning

While North Carolina's statutory exemptions offer a solid first line of defense, they have their limits. For more powerful, long-term asset protection, you need to look at estate planning tools—and that almost always means trusts. A trust is simply a legal arrangement where a third party (the trustee) holds and manages assets for someone else (the beneficiary).

When set up correctly, a trust can legally separate assets from your personal ownership. This builds a financial wall around your wealth, putting it beyond the reach of many future creditors.

Understanding Irrevocable Trusts

When we talk about asset protection, the irrevocable trust is the most powerful tool in the shed. Unlike a revocable trust, which you can change or cancel whenever you want, an irrevocable trust is designed to be permanent. Once you transfer assets into it, you give up control and ownership.

That might sound a little scary, but it’s the very thing that provides such strong protection. Since you no longer legally own the assets, they generally can't be used to satisfy a judgment against you.

Real-World Scenario:

Imagine a surgeon in Durham worried that a future malpractice claim could wipe out her personal savings. She works with her attorney to create an irrevocable trust and moves her non-retirement investment accounts into it. Years later, a lawsuit leads to a personal judgment against her. Because the assets in the trust are no longer legally hers, they are shielded and can't be seized to pay the debt, protecting her family's financial security.

This kind of proactive planning is crucial. The trust has to be created and funded before a creditor threat is on the horizon to be effective.

The Power of Spendthrift Provisions in North Carolina

What gives these trusts their teeth is a key feature called a spendthrift provision. Under North Carolina General Statute § 36C-5-502, this clause stops a beneficiary from giving away their interest in the trust. More importantly, it prevents their creditors from getting to trust assets before they are paid out.

Essentially, a beneficiary’s creditor can’t just demand payment directly from the trustee. This ensures the trust funds are used for their original purpose—to support the beneficiary—not to pay off their debts.

Key Insight: Spendthrift trusts are incredibly effective for protecting an inheritance. If you leave assets to your child in a trust with a spendthrift clause, you can help make sure that money isn't lost to their future creditors, a lawsuit, or even a messy divorce.

The North Carolina Asset Protection Trust

For a long time, you couldn't create a spendthrift trust for your own benefit (known as a "self-settled" trust) and expect it to protect you from creditors. But that has changed. North Carolina is now one of several states that allow for Domestic Asset Protection Trusts (DAPTs).

Governed by Article 6 of Chapter 36C of the General Statutes, these are special irrevocable trusts that let you be a potential beneficiary while shielding the assets from your future creditors.

These are sophisticated tools and have strict rules:

- The trust must be irrevocable.

- It must include a spendthrift clause.

- At least one North Carolina resident must serve as a trustee.

Using trusts to protect wealth is a time-tested strategy, and the financial world has taken notice. Major reports like the BlackRock Global Insurance Report show a clear trend of allocating more to private assets, a move that often goes hand-in-hand with sophisticated trust planning. For high-net-worth individuals in our state, a properly drafted North Carolina DAPT provides a powerful, statutory shield.

Trusts Also Help You Avoid Probate

On top of creditor protection, trusts offer another huge benefit: avoiding probate. Assets held inside a trust are not part of your probate estate. This means your successor trustee can manage and distribute them without court supervision after you're gone.

The process is private, much faster, and can save your family a significant amount of time, money, and stress. To get a better handle on this, you can check out our guide on how to avoid probate in North Carolina.

Advanced Strategies: Life Insurance and Business Entities

Once you've handled the basics, it's time to look at more advanced tools that can add powerful layers of protection. In our experience, properly using life insurance and formal business structures can create a serious defense against future claims.

These aren't just strategies for the ultra-wealthy. They are practical, effective tools for North Carolina business owners, real estate investors, and anyone committed to building a truly comprehensive asset protection plan.

Using Life Insurance as an Asset Shield

Most people see life insurance as a way to provide for their family after they're gone. But certain policies have significant asset protection benefits you can use during your lifetime.

North Carolina law is especially helpful here. Both the state constitution and specific statutes protect the cash surrender value and death benefits of life insurance from the policy owner's creditors, as long as the policy is payable to a spouse or children.

You can take this a step further with an Irrevocable Life Insurance Trust (ILIT). When you transfer ownership of your policy into an ILIT, you remove it from your personal estate completely. This move shields the death benefit not only from your creditors but also from your beneficiaries' future creditors and potential estate taxes. The use of insurance for financial security is a globally recognized strategy, with premiums reaching trillions worldwide, underscoring its role in legacy protection.

Creating a Liability Shield with Business Entities

If you own a business or investment properties, this is non-negotiable. Forming a separate legal entity like a Limited Liability Company (LLC) or a corporation is one of the most critical steps you can take. It builds a legal wall between your business dealings and your personal life.

This "corporate veil" means that if your business gets sued or racks up debt, creditors can generally only pursue the business's assets. Your personal home, savings, and investments stay safely on your side of that wall.

Key Takeaway: A common and costly mistake is failing to separate business and personal finances. An LLC is a straightforward and affordable way to build that liability shield—it’s absolutely essential for any North Carolina business owner.

But to keep that shield intact, you have to treat the business as a completely separate entity. That means:

- Maintaining separate bank accounts. No exceptions.

- Never co-mingling personal and business funds.

- Following all the corporate formalities your entity requires.

How This Works for Real Estate Investors

The power of this strategy really shines for real estate investors. A smart, common-sense approach is to put each investment property into its own, separate LLC.

Here’s a real-world scenario:

Let's say Mark is a real estate investor in Charlotte with three rental properties. He wisely places each house into its own individual LLC. One afternoon, a tenant at "Property A" slips on a wet step and files a major lawsuit.

Because Property A is held in its own LLC, the lawsuit is contained. The tenant's claim is limited only to the assets owned by that specific LLC—which is just Property A itself. Mark’s other two rentals, held safely in their own LLCs, are completely out of reach. More importantly, his personal home, retirement funds, and family savings are 100% protected.

This strategy effectively quarantines risk to a single asset. If Mark hadn't set this up, a single lawsuit could have threatened every business and personal asset he owned. This is a perfect example of how proper entity formation is a cornerstone of smart asset protection.

Frequently Asked Questions About Asset Protection in NC

Navigating asset protection often brings up many "what if" scenarios. We've found that getting clear, direct answers is the first step toward peace of mind. Here are some of the most common questions we hear from our North Carolina clients.

Is it too late to protect my assets if I am already being sued in North Carolina?

This is a critical concern, and timing is everything. If you start moving assets after a lawsuit has been filed or a creditor claim arises, those actions can be challenged as a "fraudulent transfer" under North Carolina's Uniform Voidable Transactions Act. A court could undo the transfer, leaving the asset exposed. However, this doesn't mean you are without options. You can still utilize your statutory exemptions (like the homestead and wildcard exemptions) to shield certain property. It is essential to consult with an attorney immediately to understand what you can still legally protect without violating the law.

Does a North Carolina divorce automatically protect my assets from my spouse's creditors?

No, a divorce does not create an automatic shield. Until your divorce is finalized, assets classified as marital property could potentially be targeted to satisfy debts incurred during the marriage, even if the debt is in your spouse's name. If you co-signed on any loans, you remain jointly responsible. A well-drafted separation agreement and final divorce decree are essential to formally sever your financial ties and protect your post-divorce assets from your ex-spouse's future creditors.

Can I use a trust to protect assets from nursing home costs in North Carolina?

Yes, this is a common and powerful strategy for long-term care planning. By transferring assets into a specifically designed irrevocable trust (often called a "Medicaid Protection Trust"), you can shield them from being counted for Medicaid eligibility. The crucial detail is that you must plan well in advance. Medicaid has a strict five-year "look-back" period in North Carolina. Any assets moved into the trust within five years of applying for Medicaid can trigger a penalty period, making you temporarily ineligible for benefits. For this strategy to work, proactive planning is non-negotiable.

Secure Your North Carolina Assets Today

Reading an online guide is an important first step, but it's not a substitute for personalized legal advice. What works for a business owner in Asheville isn't always the right strategy for a family planning their estate in Raleigh. Your financial situation is unique, and it demands a tailored plan, not a one-size-fits-all solution.

Asset protection law in North Carolina is complex, and the stakes are incredibly high. A minor misstep—like moving money at the wrong time or choosing the wrong type of trust—can lead to serious, often irreversible, legal consequences. Waiting to act is a risk you simply can’t afford to take.

Your Custom Protection Plan Awaits

Our firm is dedicated to helping North Carolina residents and their families build a secure financial future. We take the time to listen to your goals and concerns, creating a robust protection plan that fits your life and shields what you've worked so hard to earn.

We can help you navigate the legal landscape with confidence, whether you are:

- Starting or running a business

- Planning for your family’s long-term security

- Concerned about potential lawsuits or professional liability

- Looking to protect your assets during or after a divorce

A well-structured plan does more than just protect your assets; it provides invaluable peace of mind. For example, a properly established power of attorney is a critical part of any complete plan. You can learn more about how a durable power of attorney works in North Carolina in our detailed guide.

Don't leave your family’s financial future to chance. The most effective time to build your shield is now, long before a crisis appears on the horizon. By taking the initiative today, you put strong, legal protections in place for your home, your savings, and your legacy.

The decisions you make now will define your financial security for years to come. At the Law Office of Bryan Fagan, we provide the experienced legal counsel North Carolina residents need to protect their assets with confidence. Schedule a confidential consultation today to learn how we can help safeguard your future.