When people hear the word "trust," they often picture something complicated or reserved only for the extremely wealthy. The truth is, for many North Carolina families, a trust is one of the most practical and effective estate planning tools you can have. It offers peace of mind by giving you a clear, private, and powerful way to protect your legacy.

Think of a trust like a private rulebook for your assets. It’s a secure legal structure where you place your property, complete with a detailed set of instructions for a trusted person to follow on behalf of your loved ones. This is a powerful legal tool that lets you control your assets long after you’re gone, ensuring your final wishes are carried out exactly as you planned.

How Trusts Work for North Carolina Families

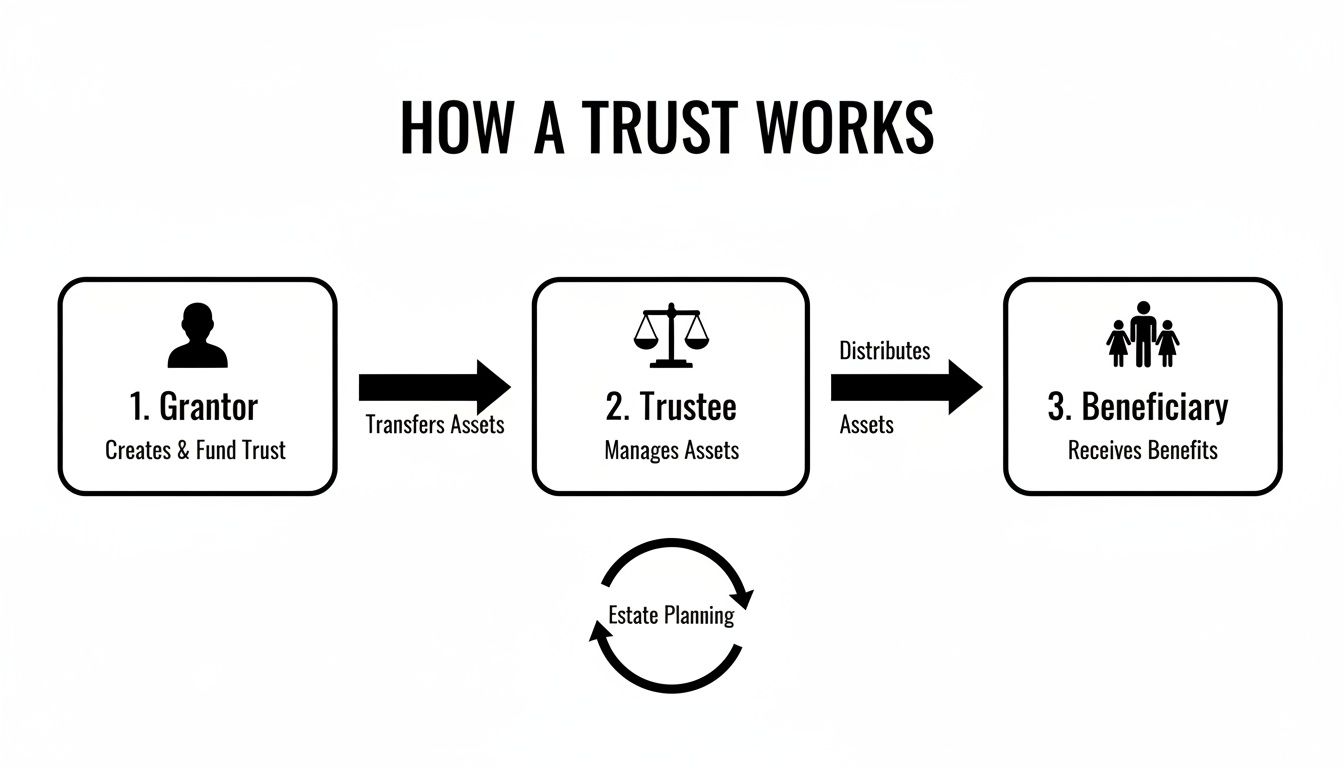

A trust is a legal relationship defined by North Carolina law, specifically the North Carolina Uniform Trust Code (Chapter 36C of the N.C. General Statutes). This arrangement always involves three key roles:

- The Grantor (or Settlor): This is you—the person creating the trust and placing your assets into it.

- The Trustee: This is the person or financial institution you appoint to manage the trust. They have a fiduciary duty under North Carolina law, meaning they must legally act in the best interests of your beneficiaries.

- The Beneficiary: These are the people or organizations who will receive the benefit of the trust’s assets, such as your children, grandchildren, or a favorite charity.

Why Do Trusts Matter for Your Family?

A trust is essentially a private contract that operates outside of the court system. One of its greatest advantages is its ability to bypass probate—the often expensive, public, and time-consuming court process for validating a will and distributing assets. If you're interested in this benefit, you can learn more about how to avoid probate in North Carolina in our detailed guide.

By placing assets like your home in Raleigh or your investment accounts into a trust, you ensure they can be managed and distributed efficiently without the typical court delays. While U.S. probate delays averaged a staggering 18 months in 2023, a well-structured trust allows for nearly immediate access and distribution for your beneficiaries when they need it most.

A trust is a powerful legal arrangement where one party, known as the trustee, holds and manages assets for the benefit of another party, called the beneficiary, as directed by the person who creates it.

This legal structure isn't new, but its modern applications have made it an indispensable tool for protecting families. The trust services market is projected to reach $15.05 billion in 2026, which shows just how vital it has become for asset protection and legacy planning. You can explore more about these trends in this overview of the trust and corporate service market. Taking these proactive steps can make a world of difference for your family during a difficult time.

How a Trust Is Created and Managed Step by Step

Understanding what a trust is conceptually is just the start. Bringing one to life is a deliberate, step-by-step process that requires careful planning and execution. Creating and managing a trust in North Carolina isn’t about signing a single paper and walking away—it involves intentional actions to build, fund, and oversee a legal structure that will protect your assets and honor your wishes for years to come.

Think of it as building a custom home for your assets. You start with a detailed blueprint (the trust document), construct the house, move your valuable belongings inside (funding), and ensure it’s properly maintained according to your rules. Let’s walk through what this looks like in practice.

Step 1: Creating the Trust Document

The first step is drafting the trust agreement. This is the legal document that acts as the rulebook for your trust, and it’s critical to work with an experienced North Carolina attorney to get it right. An online template simply cannot account for your unique family dynamics, specific assets, or long-term goals.

During this stage, you will make several key decisions:

- Appoint Your Trustee: Who will you entrust to manage your assets? This could be a responsible family member, a trusted friend, or a professional corporate trustee like a bank or trust company.

- Name Your Beneficiaries: Who will ultimately benefit from the trust? You can name individuals, like your children or grandchildren, as well as charities or other organizations.

- Set the Rules of Distribution: How and when will assets be distributed? You can specify distributions for milestones like a college graduation, a down payment on a home, or provide ongoing support for a loved one with special needs.

Real-world Scenario: A parent in Charlotte might stipulate that trust funds are to be used for their child’s education first, then for a wedding, and finally distributed outright when the child turns 30. This document is where your intentions are legally recorded and made enforceable.

Step 2: Funding the Trust

This is arguably the most important—and most often overlooked—step in the entire process. A trust document without any assets in it is like an empty vault; it provides no protection and serves no purpose. Funding the trust means legally retitling your assets into the name of the trust.

A trust only controls the assets that are legally titled in its name. If you create a trust but fail to fund it, those assets will likely still have to go through the public and lengthy North Carolina probate process.

For instance, the deed to your home in Asheville must be changed from your individual name to the name of your trust. Your brokerage account titles need to be updated, and your bank accounts may need to be retitled as well. This crucial step is what allows the trust to function as intended and keep your estate out of the courts.

The following process flow shows how the Grantor, Trustee, and Beneficiary work together within the trust structure you create.

As the visual shows, the entire structure begins with you, the Grantor. You empower the Trustee to manage assets for the ultimate benefit of your loved ones, the Beneficiaries.

Step 3: Administering the Trust

Once it’s funded, the trust becomes an active legal entity, and the Trustee's work begins. Their responsibilities are governed by both the trust document you created and the North Carolina Uniform Trust Code (N.C. Gen. Stat. Chapter 36C). This isn't a passive role; it involves active management and a legal duty to act in the best interests of the beneficiaries.

Key duties of a Trustee include:

- Prudent Investing: Managing and investing trust assets responsibly to preserve and grow their value over time.

- Making Distributions: Paying out funds to beneficiaries according to the rules you established in the trust document.

- Record-Keeping and Reporting: Maintaining detailed records of all transactions and providing regular accountings to beneficiaries so they stay informed.

- Filing Taxes: Filing annual income tax returns for the trust if it generates income.

This ongoing administration ensures your plan is executed correctly over the years, whether it involves paying for a grandchild's medical needs or managing a family business long after you're gone.

Exploring Common Types of Trusts in North Carolina

When it comes to estate planning in North Carolina, trusts are not one-size-fits-all legal documents. They are highly specific tools designed to meet unique family goals, from avoiding probate to protecting a vulnerable loved one.

Understanding the different types available is the key to building a plan that gives you true peace of mind. The most fundamental choice you will make is between a revocable and an irrevocable trust, a decision that shapes how much control you retain, the level of asset protection you get, and how your estate is ultimately handled.

Let's explore these foundational options and other specialized trusts we use to help families across North Carolina protect what matters most.

Revocable Living Trusts: The Flexible Foundation

A Revocable Living Trust is the most common type of trust for one simple reason: it offers maximum flexibility. When you create a revocable trust, you typically name yourself as the initial trustee. This means you maintain complete control over the assets you place inside it.

You can buy or sell property held by the trust, change the beneficiaries, or even dissolve the trust entirely at any time. Think of it as a personal container for your assets that you can rearrange whenever your circumstances change. Its primary purpose is to hold your assets so they can pass to your heirs privately and efficiently, completely bypassing the North Carolina probate court process.

Real-World Scenario: A retired couple in Raleigh owns their home, a vacation property, and several investment accounts. By placing these assets into a revocable living trust, they continue managing them just as they always have. When they pass away, their designated successor trustee immediately steps in to distribute the property to their children according to the trust's instructions, avoiding months of court proceedings.

Irrevocable Trusts: The Protective Fortress

In contrast, an Irrevocable Trust is built for permanence and protection. Once you create and fund an irrevocable trust, you generally cannot change or revoke it without the consent of your beneficiaries. You give up direct control over the assets, which are now managed by a trustee you appoint.

So, why would anyone willingly give up that control? The answer lies in the powerful benefits this structure provides. Because the assets are no longer legally yours, they are shielded from your personal creditors and lawsuits. Crucially, this type of trust can also be structured to help you qualify for long-term care benefits like Medicaid without depleting your life savings.

An irrevocable trust creates a legal separation between you and your assets. This separation is what provides a powerful shield against creditors and is a vital component of long-term care planning.

This is a strategic tool for asset preservation. If you're concerned about future liabilities or the high cost of nursing home care, an irrevocable trust is a conversation worth having. For those wanting to delve deeper, our firm has published a guide on how to protect assets from creditors that you may find helpful.

Revocable vs. Irrevocable Trusts: A North Carolina Comparison

To help you visualize the trade-offs, here’s a straightforward comparison of the two main trust categories. Understanding these key differences is the first step in deciding which structure aligns with your estate planning goals in North Carolina.

| Feature | Revocable Trust | Irrevocable Trust |

|---|---|---|

| Flexibility | High. Can be changed or canceled by the creator at any time. | Low. Cannot be easily changed or canceled once created. |

| Control | Creator retains full control as trustee. | Creator gives up control to an appointed trustee. |

| Probate Avoidance | Yes. Assets in the trust bypass probate. | Yes. Assets in the trust bypass probate. |

| Asset Protection | No. Assets are still considered yours and are vulnerable to creditors. | Yes. Assets are legally separated and protected from your creditors. |

| Estate Tax | Assets remain part of your taxable estate. | Assets are typically removed from your taxable estate. |

| Medicaid Planning | No. Assets are counted when determining eligibility. | Yes. Can be structured to protect assets for long-term care eligibility. |

While a revocable trust offers unparalleled control for managing assets during your lifetime and avoiding probate, an irrevocable trust provides robust protection that a revocable trust simply cannot. The right choice depends entirely on your priorities for asset management, creditor protection, and legacy planning.

Specialized Trusts for Unique Family Needs

Beyond these two main categories, North Carolina law allows for specialized trusts to address specific family situations. These trusts show just how adaptable estate planning can be when tailored to your life.

Testamentary Trusts: Unlike a living trust created during your lifetime, a testamentary trust is established through the terms of your will. It only comes into existence after you die and your will goes through probate. This is often used to manage inheritances for minor children or for an adult beneficiary who may not be ready to handle a large sum of money.

Special Needs Trusts (SNTs): This is a life-changing tool for families with a disabled loved one. An inheritance left directly to a person receiving government benefits like Supplemental Security Income (SSI) or Medicaid could disqualify them from that essential aid. A Special Needs Trust holds the inheritance for their benefit, allowing the trustee to pay for supplemental needs—like education, travel, or medical care not covered by benefits—without jeopardizing their eligibility.

Real-World Scenario: A Charlotte family has an adult child with a developmental disability who relies on Medicaid. They create a Special Needs Trust within their estate plan. When they pass away, their child's inheritance flows into the SNT, ensuring they have resources to enhance their quality of life while remaining fully eligible for the government support they depend on.

Each of these trusts serves a distinct purpose. Choosing the right one requires a clear understanding of your assets, family dynamics, and long-term goals.

Choosing Between a Trust and a Will in North Carolina

One of the most important questions we hear from North Carolina families is, "Do I really need a trust if I already have a will?" It's a great question, and understanding the answer is critical. Wills and trusts serve very different functions, and the choice you make can dramatically change how your legacy is managed and how quickly your loved ones get the support they need.

Think of a will as a set of instructions for the North Carolina probate court. After your passing, your will becomes a public document that a judge uses to oversee how your assets are distributed. This court-supervised process, known as probate, is often slow, can be quite expensive, and puts your family's financial affairs on public display.

A trust, on the other hand, is a private agreement that works outside the courtroom. When it’s properly funded, it allows your hand-picked trustee to manage and distribute your assets immediately, privately, and precisely according to your wishes—no judge’s permission needed.

When a Will Might Be Enough

For some folks, a simple will is a perfectly fine solution. If your estate is small, you don't have many assets, and you don’t own any real estate like a house or land, a will can get the job done. It’s a straightforward and often cost-effective way to handle uncomplicated financial situations.

Just remember, even with a will, your estate will still have to go through the North Carolina probate process. For many families, avoiding that public process for their loved ones is a top priority. If you're just starting to plan, you can explore our North Carolina will template to see what goes into this foundational document.

When a Trust Becomes Essential

This is where a common myth gets busted: trusts are not just for the ultra-wealthy. In reality, they are practical tools that solve common problems for everyday North Carolina families.

A trust becomes an invaluable tool if you:

- Own a home or other real estate: Putting property into a trust is one of the best ways to ensure it passes to your heirs without getting stuck in probate for months on end.

- Want to keep things private: A will and the entire probate process are public records. A trust keeps your family’s financial matters and distributions completely private.

- Need to protect your beneficiaries: With a trust, you can set conditions for an inheritance. This is perfect for protecting assets for a young adult, a loved one who isn't great with money, or a family member with special needs.

The numbers back this up. Trusts can speed up asset distribution by up to 75% compared to the probate timeline. Research also shows they can slash administrative costs by as much as 70%, leaving more of your legacy for your family.

The Pour-Over Will: A Critical Safety Net

Here's an important point: creating a trust doesn't mean you should throw out the idea of a will. In fact, a special kind of will, called a pour-over will, works hand-in-hand with your trust to act as a crucial safety net.

A pour-over will is designed to "catch" any assets that you may have forgotten to fund into your trust or acquired shortly before your passing. It simply states that any assets left in your individual name should be transferred—or "poured over"—into your trust upon your death.

This simple document ensures that everything you own is ultimately managed under the private and efficient rules you laid out in your trust. It closes any potential gaps in your estate plan, providing full protection and making sure your final wishes are honored. Without a pour-over will, any assets left out of the trust would be forced into North Carolina's public probate system.

How Trusts Affect Divorce and Asset Protection

For many North Carolina families, a trust isn't just about planning an inheritance. It’s a critical shield for protecting your assets against life’s most stressful and unexpected turns. Two of the biggest concerns we hear from clients are how to guard their wealth against future creditors and what happens to a trust if they get divorced.

Knowing how trusts work with North Carolina law in these situations is the key to real asset protection. A properly structured trust can mean the difference between keeping your assets secure and watching them get exposed to claims or divided in a divorce.

Trusts and North Carolina Divorce Law

When a marriage ends in North Carolina, the court divides marital property through equitable distribution, a process detailed in N.C. Gen. Stat. § 50-20. The first step is to classify every asset as either marital, separate, or divisible. The classification of assets held in a trust is one of the most complex issues that can come up in a divorce.

The deciding factor usually boils down to the type of trust you have and when it was created.

- Assets in a Revocable Trust: Property held in a revocable living trust is almost always considered marital property if it was earned or placed in the trust during the marriage. Since the person who created it (the grantor) can change or even cancel the trust at any time, they still have control. Courts typically see these assets as part of the marital estate and subject to division.

- Assets in an Irrevocable Trust: A well-drafted irrevocable trust offers much stronger protection, especially if it was set up before the marriage or funded with clearly separate property (like an inheritance). Because you give up control of the assets to a trustee, they are legally no longer yours. This means they can be classified as separate property, shielding them from equitable distribution.

Real-World Scenario: Imagine a Charlotte business owner who created an irrevocable trust for his children years before getting married. He funded it with shares of his company. When he later divorces, those shares are locked inside the trust, legally separate from his personal and marital finances. As a result, they are protected and not up for division with his spouse.

Protecting an Inheritance from Division

One of the most common worries clients bring to us is protecting an inheritance from a potential divorce. While North Carolina law considers an inheritance to be separate property, it can easily lose that status if it gets commingled, or mixed, with marital money.

A trust is the best tool available to prevent commingling. By placing your inheritance directly into a dedicated trust, you create a clear legal boundary around those funds. This preserves their identity as separate property and keeps them from being divided in a divorce.

Using Trusts for Creditor and Lawsuit Protection

Beyond divorce, certain trusts provide a powerful shield against creditors and lawsuits. This is a vital strategy for professionals in North Carolina like doctors, architects, and business owners who face a higher-than-average risk of liability. A revocable trust offers no protection here; since you still control the assets, creditors can get to them.

An irrevocable trust, however, can provide serious asset protection. When you transfer assets into a properly structured irrevocable trust, you legally remove them from your personal ownership. This makes it incredibly difficult for future creditors to seize those assets to satisfy a judgment against you. This kind of proactive planning can secure your family’s financial future from unforeseen professional risks.

Secure Your Legacy with a North Carolina Trust Attorney

Understanding the mechanics of a trust is one thing, but putting that knowledge into practice to build a plan that truly protects your family is another. Throughout this guide, we've explored how a trust can help you avoid the public, costly probate process and give you lasting control over your legacy.

But this isn't the time for a do-it-yourself approach. Relying on generic online templates is one of the most common—and costly—mistakes we see. Those one-size-fits-all documents often create the exact legal battles, financial drain, and family conflict they were supposed to prevent. Your family's situation is unique, and your estate plan needs to be built specifically for you.

Why You Need a North Carolina-Specific Plan

Navigating North Carolina's distinct trust laws, property codes, and asset protection rules demands more than just filling in blanks on a form. An experienced North Carolina trust attorney does more than draft documents—we build a strategy. We take the time to understand you, your family dynamics, and your goals to create a plan that works in the real world.

True peace of mind comes from knowing your plan isn't just legally valid, but strategically built to protect your family from the unexpected. A well-crafted trust is your strongest defense.

A properly designed North Carolina trust can:

- Avoid Probate: Keep your estate out of the courts, ensuring your assets are distributed privately and efficiently without unnecessary delays and fees.

- Protect Beneficiaries: Safeguard an inheritance for young adults, loved ones with special needs, or anyone who might need help managing their funds.

- Shield Assets: Create a strong legal barrier to help protect your family’s inheritance from creditors or future lawsuits.

- Maintain Control: Set clear rules for how, when, and to whom your assets are distributed, ensuring your wishes are followed for years to come.

Don’t leave your family’s financial security to chance. At the Law Office of Bryan Fagan, we are dedicated to helping North Carolina families build the legal foundation they need to protect what matters most.

We invite you to take the next step. Schedule a consultation with our experienced North Carolina estate planning team today to discuss how we can help you build a plan that provides genuine security for you and your loved ones.

Frequently Asked Questions About Trusts in North Carolina

When you start digging into how a trust works, a lot of specific questions are bound to come up. To give you some clarity, we’ve put together answers to the questions we hear most often from our North Carolina clients.

Do I Still Need a Will if I Have a Trust in North Carolina?

Yes, absolutely. A well-designed estate plan that uses a trust should always include a companion document called a pour-over will. Think of this will as a critical safety net.

Its main job is to "catch" any assets that were accidentally left out of your trust or that you acquired right before your death. The will then directs—or "pours"—those assets into your trust. This ensures they are managed according to your private wishes and aren't left stranded in the public North Carolina probate system.

How Much Does It Cost to Create a Trust in North Carolina?

Setting up a trust does have a higher upfront cost than just drafting a simple will. However, it's a mistake to see this as just an expense. It's an investment in protecting your estate and your family.

The costs tied to the North Carolina probate process—court fees, executor pay, and legal bills—are often far higher than the initial cost of creating a trust. By planning ahead with a trust, you are essentially pre-paying to help your family avoid the much bigger financial and emotional toll of probate down the road. While we cannot guarantee specific outcomes or costs, a consultation can help clarify the investment for your unique situation.

Can a Revocable Trust Help Me Qualify for Nursing Home Care in NC?

This is a critical and very common misunderstanding. A revocable living trust provides zero asset protection when it comes to planning for Medicaid long-term care in North Carolina.

Because you keep full control over the assets in a revocable trust, the state of North Carolina sees them as completely available to you. They will be counted when determining if you are eligible for benefits. To shield assets from nursing home costs, a very specific type of irrevocable trust is required, and it demands careful, strategic planning well in advance—usually five years or more—to be effective.

Does My Trust Need Its Own Tax ID Number?

That depends entirely on the kind of trust you have.

- A revocable living trust is directly tied to you. For tax purposes, it simply uses your own Social Security Number. Any income the trust assets generate is reported on your personal tax return.

- An irrevocable trust is treated as a separate legal and taxable entity. It must get its own tax ID number, called an Employer Identification Number (EIN), from the IRS. It will also be required to file its own annual tax returns.

Navigating North Carolina's trust laws requires a skilled hand and a strategic plan. The decisions you make today will have a lasting impact on your family's future. At the Law Office of Bryan Fagan, we are committed to helping you build a secure legacy. Schedule a consultation with our experienced North Carolina estate planning team to get started.