Thinking about what happens after you're gone is never easy, but proactive estate planning is one of the most profound gifts you can give your family. Here in North Carolina, one of the primary goals of a well-crafted plan is learning how to avoid probate. This isn't about finding secret loopholes; it's about using established legal tools like revocable living trusts and proper beneficiary designations to ensure your assets pass directly to your loved ones, privately and efficiently, without court interference.

What Is North Carolina Probate and Why Should You Avoid It?

So, what exactly is probate? In simple terms, it's the formal court-supervised process for validating a will, paying off final debts, and distributing a person's assets after they die. It sounds straightforward, but for many North Carolina families, the reality is a frustrating, expensive, and public affair.

The moment an estate enters probate, it ceases to be a private family matter. The Clerk of Superior Court in your county oversees the entire process. Every action, from appointing an executor to selling a car to pay a bill, requires court approval and becomes a public record. Understanding this is the first step in realizing why avoiding probate is so crucial for protecting your family’s privacy and inheritance.

The Real Cost of Probate: It’s More Than Just Money

Many are shocked by the direct financial toll an estate takes during probate. These aren't minor administrative fees; they can significantly shrink the inheritance you worked so hard to build for your family.

To put it in perspective, here’s a breakdown of what a North Carolina estate can expect to lose.

The Real Cost of Probate in North Carolina

| Probate Element | Typical Impact in North Carolina |

|---|---|

| Executor Commission | Under N.C.G.S. § 28A-23-3, the court can approve a commission of up to 5% of the estate's receipts and disbursements. On a $500,000 estate, that's potentially $25,000 right off the top. |

| Attorney's Fees | Most executors need legal guidance to navigate the complex process, adding thousands more in hourly or flat fees. |

| Court Costs & Filing Fees | Filing petitions, paying the "inventory tax" on assets, and other court-mandated fees add up quickly. |

| Total Drain | It’s common for probate to consume 3% to 7% of an estate's total value before a single heir receives their inheritance. |

These costs are paid directly from the estate's funds, meaning your family ultimately bears the financial burden of a public process you could have helped them avoid.

The Agonizing Wait: Frozen Assets and Frustrating Delays

Beyond the financial cost is the frustratingly slow pace of probate. It is not a matter of weeks. In North Carolina, even a "simple" probate can easily take six months to a year, and complex estates can drag on much longer.

During this entire period, many of the estate's assets are essentially locked down. Bank accounts can be frozen, and real estate cannot be sold or refinanced without court permission.

Real-World Scenario: Imagine a father in Charlotte passes away. His will leaves everything to his daughter, including a $200,000 brokerage account. Because the account was titled only in his name, it's a probate asset. His grieving daughter can’t access those funds for months. She’s left trying to cover funeral costs and the mortgage on her dad's house out-of-pocket. This type of financial strain is incredibly common and entirely preventable with proper planning.

A Public Spectacle: The Loss of Family Privacy

Finally, probate is public. When an estate goes through probate in North Carolina, the will, a complete inventory of assets, and a list of all debts become part of the public record at the county courthouse.

This means anyone—a curious neighbor, a disgruntled relative, or a predatory salesperson—can look up:

- A detailed inventory of everything you owned.

- How much debt you carried.

- Who inherited your assets and exactly how much they received.

For most families, this feels like a profound invasion of privacy during an already vulnerable time. Planning to avoid probate keeps your family's financial affairs exactly where they belong: private.

To get a better sense of the official steps your family could be forced to navigate, you can read our detailed guide on the North Carolina probate process.

The Revocable Living Trust: Your Strongest Tool

When clients in North Carolina ask me how to keep their estate out of court, the conversation almost always turns to one incredibly effective tool: the revocable living trust.

Think of it as a private legal container you create to hold your most important assets—your home, investment portfolios, and bank accounts. It’s a cornerstone strategy for avoiding probate, and for good reason.

While you're alive and well, you remain in complete control. You act as the grantor (the person who creates the trust) and the trustee (the manager). This means you can manage, buy, and sell assets inside the trust just as you always have. Your day-to-day life doesn't change.

The magic happens upon your incapacity or death. Your designated successor trustee—a person or institution you trust—can step in immediately to manage or distribute the assets according to your private instructions. No court approval is needed, and the entire public probate process is bypassed.

The Critical Importance of Funding Your Trust

Here's the catch, and it's a big one: creating the trust document is only half the battle. A trust without assets is just an empty legal shell. The process of legally transferring your assets into the trust is called funding, and failing to do it is one of the most common and heartbreaking mistakes I see.

Real-World Scenario: A Tale of Two Trusts

I've seen this play out time and again. Imagine two neighbors in Raleigh. The first family, the Jacksons, diligently worked with their lawyer to retitle their house, brokerage account, and savings into their trust's name. When they passed, their son, as successor trustee, settled their final affairs and distributed their inheritance in just a few weeks.Down the street, the Smiths signed their trust documents and put them in a drawer. They never got around to funding it. Their home, their bank accounts—everything was still in their individual names. After they died, their kids were shocked to learn the trust was legally empty. Every single asset had to be dragged through the full North Carolina probate process, completely defeating the purpose of all their planning.

This story illustrates a non-negotiable truth: an unfunded trust provides zero protection from probate.

How to Fund Your North Carolina Trust

So, what does funding a trust actually involve? It means officially changing the legal owner of an asset from you, the individual, to you, as the trustee of your trust. It requires some specific paperwork, but it’s a straightforward process with professional guidance.

Key Assets to Transfer:

- North Carolina Real Estate: This is vital. You’ll need a new deed prepared by an attorney to transfer your home, vacation property, or rental real estate from your name into the trust. The ownership would change from "John and Jane Doe" to "John and Jane Doe, Trustees of the Doe Family Revocable Living Trust."

- Bank and Brokerage Accounts: You will work with your financial institutions to fill out their specific forms to retitle your checking, savings, and non-retirement investment accounts into the name of the trust.

- Business Interests: If you own a piece of an LLC or another business, that ownership interest can and should be assigned to your trust.

It's equally important to know what not to put in your trust. Assets like IRAs and 401(k)s have special tax-deferred status and should not be retitled into a trust. You'll handle those with beneficiary designations, which we’ll discuss next. As you work on your estate plan, you may also want to review our guide on how to protect assets from creditors to create an even stronger financial shield.

Beyond probate avoidance, a living trust offers another crucial benefit: incapacity planning. If you ever become unable to manage your own finances due to illness or injury, your successor trustee can step in immediately to pay bills and manage your assets without the need for a costly and public court-ordered guardianship. This dual protection makes it an essential component of any solid North Carolina estate plan.

Using Beneficiary Designations for a Direct Transfer

Not every asset needs to be placed in a trust to sidestep the headaches of probate. In fact, one of the simplest and most powerful tools for avoiding court oversight is likely something you already have: a beneficiary designation. Think of it as a direct instruction, ensuring your money goes straight to your loved ones without ever touching a probate court file.

Here in North Carolina, these designations are a binding contract between you and your financial institution. When you pass away, that institution is legally obligated to transfer the asset to the person you named. This happens completely outside of your will and the probate process.

How POD and TOD Designations Work

You'll usually see these referred to as Payable-on-Death (POD) for bank accounts (like checking and savings) or Transfer-on-Death (TOD) for investment and brokerage accounts. The names differ, but the goal is identical: a seamless, private transfer.

Setting them up is almost always simple. It usually involves filling out a one-page form provided by your bank or financial advisor. You will name a primary beneficiary and, just as importantly, a contingent (or secondary) beneficiary in case your first choice is unable to inherit.

Real-World Scenario: I once worked with a client in Asheville who was concerned her children wouldn't have immediate cash for her final expenses. She knew if her checking account got tied up in probate, the money could be frozen for months. We simply helped her add POD designations to her bank accounts, naming her two children as equal beneficiaries. After she passed, all her children needed was a death certificate to show the bank, and they had access to the funds within days. It provided critical relief at an incredibly stressful time.

This immediate access is precisely why beneficiary designations are so valuable. A will initiates the probate process; a beneficiary form sends your assets directly to your family.

Assets That Can Bypass Probate This Way

This strategy is incredibly flexible and works for some of the most common and valuable assets people own. It's a fundamental piece of the puzzle when learning how to avoid probate for a significant part of your estate.

You can and should use beneficiary designations for:

- Life Insurance Policies: The death benefit is almost always paid directly to the named beneficiary, not the estate.

- Retirement Accounts: This is crucial for IRAs, 401(k)s, 403(b)s, and similar plans.

- Bank Accounts: Your checking, savings, money market accounts, and CDs can all have POD beneficiaries.

- Investment Accounts: Stocks, bonds, and mutual funds held in brokerage accounts can have TOD beneficiaries.

This powerful, direct-transfer method is why proper estate planning is so critical. Yet, while most people agree planning is important, a shocking number of Americans don't even have the basics in place, leaving their families to deal with North Carolina's default intestacy laws. You can discover more insights about why so many people are unprepared on bordenlawnv.com.

The Critical Need for Regular Reviews

Here’s a warning I give every client: beneficiary designations are not a "set it and forget it" task. Life changes, and if your forms don't change with it, you can create a real mess for your family.

Any of these major life events should trigger an immediate review of all your beneficiary forms:

- Marriage or divorce

- The birth or adoption of a child

- The death of a person you've named as a beneficiary

- A major falling out or change in your relationship with a beneficiary

I've seen firsthand what happens when these forms are neglected. An ex-spouse inherits a 401(k), or a deceased child's share gets paid to their own estate—landing it right back in the probate court you were trying so hard to avoid. A quick annual review is all it takes to make sure your assets go to the right people, at the right time, without a fight.

How Property Ownership Can Bypass Probate

Sometimes the simplest strategies are the most effective. When it comes to estate planning, how you title your property—the actual names on a deed or bank account—can be one of the most powerful tools for avoiding probate. With the right legal language, you can ensure an asset transfers directly to a co-owner, completely bypassing the court system.

This all comes down to a legal principle known as the right of survivorship.

Think of it this way: when one owner passes away, their share automatically and immediately belongs to the surviving owner(s). It's that simple. The asset never technically enters the deceased's estate, which means it stays out of probate court.

Joint Tenancy with Right of Survivorship

In North Carolina, the most direct way to establish this is with a Joint Tenancy with Right of Survivorship (JTWROS). But there's a critical detail: the legal document, like a property deed, must contain that exact language: "as joint tenants with right of survivorship." If that specific legal phrase isn't there, North Carolina law defaults to a different kind of ownership ("tenancy in common") that does not skip probate.

Details like this are everything. A simple wording error can unravel an entire plan. With over 1.2 million U.S. estates projected to hit the probate courts annually by 2026, getting the North Carolina-specific details right is non-negotiable. You can discover more about these NC-specific estate strategies from Larson Brown Law.

A Special Protection for Married Couples: Tenancy by the Entirety

For married couples in our state, North Carolina law provides an even better option: Tenancy by the Entirety. This form of ownership is exclusive to spouses and automatically includes the right of survivorship. When one spouse dies, property they own together passes instantly to the surviving spouse without ever seeing the inside of a probate court.

But Tenancy by the Entirety offers another incredible benefit: powerful creditor protection.

Real-World Scenario: A Raleigh couple, David and Sarah, own their home as "tenants by the entirety." David, a small business owner, unfortunately faces a lawsuit that results in a personal judgment against him. Because the house is legally owned by the marital unit—not just David as an individual—his creditor cannot force the sale of the home to satisfy his separate debt. This protection is invaluable and unique to this type of ownership.

If David were to pass away, Sarah would become the sole owner of the home, free and clear of probate. Plus, the property would still be protected from David's old individual creditors. This one-two punch of probate avoidance and asset protection makes it a foundational strategy for married couples in North Carolina.

The Risks and Downsides of Joint Ownership

While it sounds straightforward, joint ownership isn’t a one-size-fits-all solution. In fact, it can create serious problems if you’re not careful. The moment you add another person (other than a spouse) to your title, you give up exclusive control.

Before you go this route, consider the very real downsides:

- Loss of Control: You can no longer sell or mortgage the property on your own. You need your co-owner’s signature for everything. It's now their asset, too.

- Creditor Exposure: If your co-owner gets divorced, files for bankruptcy, or is successfully sued, your property is now on the line. Their financial troubles have become your problem.

- Unintended Consequences: Adding a child to a deed might seem like a simple way to pass on the family home, but it can trigger gift tax issues and often leads to bitter family disputes down the road.

Because these risks are so significant, joint ownership should be used with extreme caution. For many people, a revocable living trust is a far more flexible and secure way to transfer assets, as it allows you to maintain full control throughout your life while still ensuring your property avoids probate.

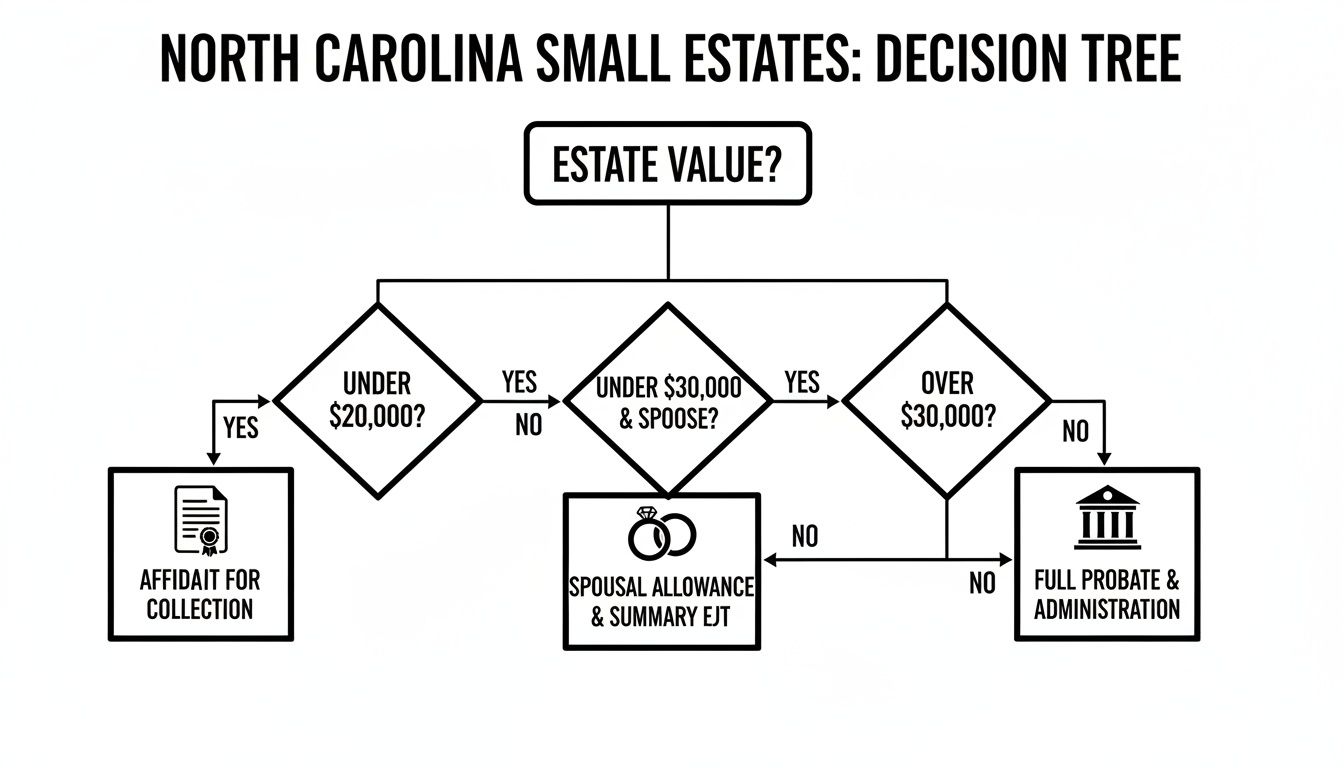

What If My Estate Is Small? North Carolina's Simplified Procedures

Sometimes, no matter how well you plan, a few assets might still need to go before the court. The good news? That doesn't automatically mean your family is in for the full, drawn-out probate process. For smaller estates in North Carolina, the law provides a couple of valuable shortcuts.

Think of these as an important safety net. They can save your loved ones a world of time, expense, and headaches if your estate happens to fall below certain monetary thresholds.

Collection by Affidavit: The Go-To for Smaller Estates

The most frequently used shortcut is known as Collection by Affidavit, or what many lawyers simply call a small estate affidavit. This process is laid out in Chapter 28A, Article 25 of the N.C. General Statutes, and it’s a game-changer. It allows an heir to collect and distribute a loved one's personal property without the formal need to be appointed as an executor by the court.

To use this simplified method, the total value of the deceased's personal property (after subtracting any liens and debts) must be under a specific amount:

- $20,000 if the decedent was unmarried.

- $30,000 if the surviving spouse is the sole heir of the estate.

Now, here’s a critical detail: this process is strictly for personal property. That includes things like bank accounts, cars, stocks, and furniture. It absolutely cannot be used to transfer real estate.

Here’s how it works in practice: Let's say a father in Greensboro passes on, leaving a checking account with $15,000 and a car worth $4,000. His daughter is his only heir. Since his total personal property is $19,000—well under the $20,000 limit—she can use a Collection by Affidavit. She'll file the proper form with the Clerk of Superior Court. Once it's approved, she can take that official document to the bank and the DMV to get the assets transferred directly into her name, completely bypassing full probate.

Summary Administration: A Direct Path for Spouses

There's another express lane available called Summary Administration. This option, however, is very specific: it can only be used when the surviving spouse is the one and only heir of the entire estate. This could be because the will leaves everything to them, or because they inherit everything under North Carolina's intestacy laws if there is no will.

With Summary Administration, the surviving spouse simply files a petition with the court. After the court verifies that the spouse is indeed the sole inheritor, it can issue a direct order. This order releases all the estate property to them, cutting out the long and winding road of traditional probate.

While these procedures are incredibly useful, they aren't a substitute for a comprehensive estate plan. Relying on them is a gamble, as your estate's eligibility depends on its value when you pass away—something no one can predict. A secure plan built with tools like trusts and proper beneficiary designations ensures your assets stay out of court, regardless of their final value.

Putting It All Together: Building Your North Carolina Estate Plan

You now have a solid understanding of the tools available to keep your estate out of the North Carolina court system. The best strategy always comes down to your unique situation—your assets, your family dynamics, and your personal goals.

A common misconception is that estate planning is only for the wealthy. In truth, it’s often more critical for families with modest estates. For them, the thousands of dollars and months of time lost to probate aren't just an inconvenience; they can be a significant financial blow.

Take Action to Secure Your Legacy

For smaller estates, North Carolina does offer some simplified procedures, but relying on them is a risk. This decision tree illustrates how the process can unfold.

As you can see, everything hinges on the estate's value at the time of death. If it falls below the threshold, your loved ones might be able to use a streamlined affidavit. But if it's even one dollar over, they could face full, formal administration. Since you can't predict your estate's exact value down the road, proactive planning is always the smarter, safer route.

Don't let the details paralyze you. While it’s great to be informed, a DIY approach to estate planning can backfire spectacularly. I’ve seen cases where a small mistake in a self-drafted will or trust completely invalidated the document, forcing the family right back into the probate process they were trying to avoid. You can read more about the details required in a North Carolina Will Template to see just how complex it can be.

The most important step you can take is to get personalized advice from an experienced North Carolina estate planning attorney. A professionally crafted plan is truly one of the greatest gifts you can leave your family.

Frequently Asked Questions About Avoiding Probate in NC

When individuals and families come to our office, they often have similar questions and concerns. It's completely understandable—this can be a confusing process. Here are answers to some of the most common questions we hear from clients across North Carolina.

If I have a will, do I avoid probate?

This is the single most common misconception about estate planning. A Last Will and Testament does not avoid probate; it guarantees it. A will is simply a set of instructions for the probate court. When you pass away, your will is filed with the Clerk of Superior Court to begin the probate process. To actually bypass the court system, its costs, and its public nature, you need tools like a revocable living trust, beneficiary designations, or proper property titling.

What is the main difference between a will and a living trust?

The key difference is court involvement. A will is a public document that only goes into effect after you die and must be validated by the probate court. A revocable living trust is a private document that you control during your lifetime and that allows for the immediate, private transfer of your assets upon your death by your chosen successor trustee, without any court oversight. A trust can also manage your assets for you if you become incapacitated, a benefit a will does not provide.

Can I just add my child's name to my house deed to avoid probate?

While technically adding a child as a "joint tenant with right of survivorship" will keep that one asset out of probate, it is an extremely risky strategy. The moment you add their name, you give up exclusive control of your home. Worse, if your child gets divorced, is sued, or files for bankruptcy, your home is now exposed to their creditors. A revocable living trust achieves the same probate-avoidance goal without sacrificing control or exposing your most valuable asset to these significant risks.

Secure Your Family's Future Today

Your family's financial security is too important to leave to chance or to the default rules of the North Carolina probate court. The decisions you make today will directly impact the people you care about most during a difficult time.

We understand that this process can feel overwhelming. Our team is here to provide clear guidance and empathetic support. Schedule a confidential consultation with the Law Office of Bryan Fagan to discuss your specific situation. Let us help you build a personalized estate plan that protects your assets, provides for your loved ones, and gives you invaluable peace of mind.

Contact us today at https://bryanfaganlaw-nc.com to take the first step.